Published 16 January 2020

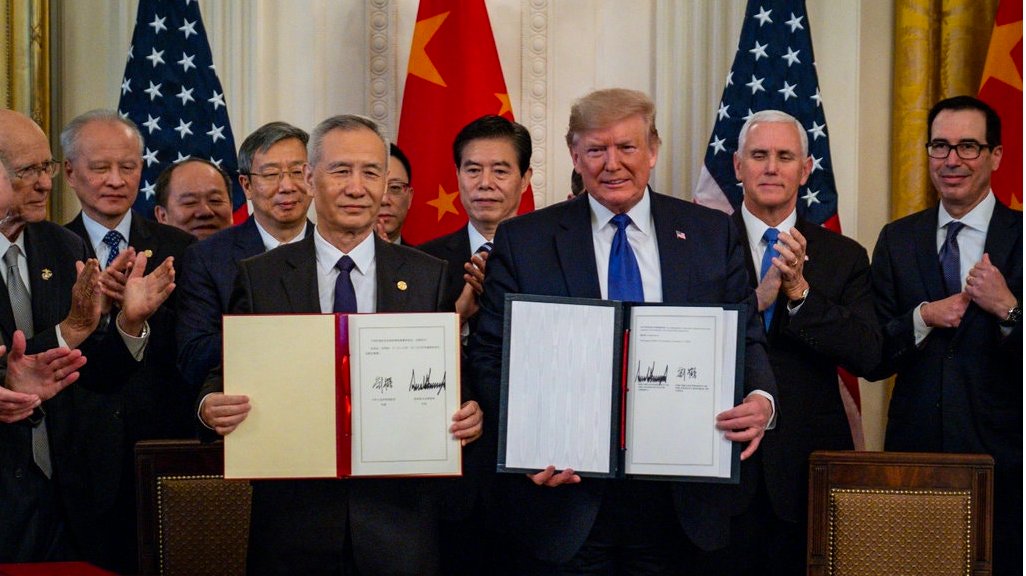

The United States and China have finally signed an agreement intended to stop escalation of the ongoing trade and tariff war and lock in certain commitments to avoid a repeat. The deal represents “Phase 1” of resolving challenges in the overall bilateral relationship.

Phase 1 contains pledges in a variety of areas, including intellectual property rights, financial services, and technology transfer. It also includes specific purchase targets for up to $200 billion in American agriculture, machinery and energy products.

The agreement is already being criticized on many fronts, including the irony of asking China to follow free-market principles while simultaneously embedding pure managed trade commitments, the challenges of meeting the purchasing targets, and the apparent “re-packaging” of a host of commitments by China made over decades.

This Talking Trade, however, is more interested in what the agreement means for Asia.

For two years, the US and China have been engaged in rapid escalation of tensions. The most obvious sign of the unraveling relationship has been the imposition of tariffs by both sides.

The Phase 1 deal only begins to scratch the surface of these tariffs. The US has promised not to impose tariffs on every single item coming in from China (culminating in List 4B, which remains suspended under the Phase 1 deal) and to reduce tariffs currently set at 15% to 7.5% on roughly $120 billion of additional goods (List 4A).

Tariffs on the remaining $250 billion of Chinese exports to the US (Lists 1-3) will remain at 25% for the foreseeable future. Chinese tariffs on nearly all US imports may be selectively removed, particularly where needed to allow increased purchases of scheduled American products.

The past two years have also seen an increasing level of scrutiny of Chinese investments into the United States, including the implementation of two new regulations under the Committee on Foreign Investment in the United States (CFIUS). Largely as a result, Chinese investment in the US has plunged. Tightened investment restrictions in the United States are not addressed in the Phase 1 agreement.

The US has also expanded the range and reach of the “entities list,” with a plan in place to continue screening Chinese inputs into other supply chains. The US has also increased scrutiny on Chinese scholars and academics.

One important element that was meant to be addressed through the escalating trade war were China’s vast subsidy programs. These subsidies, typically funneled through a variety of state-owned enterprises, are assumed to be causing market distortions and oversupply of important products like steel which are then dumped onto global markets. The Phase 1 deal did not address these.

The agreement signed yesterday in Washington is therefore meant to be the start of a process of resetting the bilateral relationship. Many of the toughest issues, like tackling subsidies, are now supposed to be covered in a Phase 2 negotiation.

Companies seem to have expected that Phase 2 talks would begin immediately. However, early signs from Washington suggest that these negotiations may not get underway until 2021. At a minimum, all of the existing tariffs on bilateral trade will remain in place at least through the remainder of this year.

Only after the US Presidential elections in November, or after inauguration in January (if Trump is defeated), will firms be able to realistically consider tariff relief. Talks on other elements of the contested US-China relationship may be tackled at that time.

Phase 1 includes an enforcement mechanism, but it is a highly unusual process that delivers significant power to both parties to unilaterally change the terms at almost any time. It practice, it means that President Trump could opt to reimpose tariffs on all Chinese goods, raise tariff rates, or engage in any number of punishment actions.

This is particularly true given the difficulties that China is likely to have in meeting the agreed purchase targets. The amounts in question for buying agricultural and other goods can represent a doubling of any previous high water mark for Chinese purchases. China is likely to be “out of compliance” with Phase 1 in the very near term, leaving open the potential for US sanctions at any time.

What does this mean for Asia? At least three things seem obvious.

First, the tariff pressures are going to remain for companies. Not only are firms still subject to extensive tariffs, but the risk of future increases is only marginally reduced. In the very best case scenario, firms will continue to pay 25% tariffs for another 10 months.

Companies may not be able to weather this extent of damage for so much longer. Many companies will finally pull the trigger on relocation plans. Most of the supply chain adjustment will not be redirected back to the United States, but will be shuffled around globally. Many Asian markets are obvious places for moving manufacturing.

Second, the restrictions on Chinese investment into the US will remain in place. Chinese investment dollars are likely to be redirected, including into other Asian markets. The impending start of the Regional Comprehensive Economic Partnership (RCEP) will accelerate this trend.

Third, the Phase 1 deal only begins to scratch the surface of looming technology conflicts. The placement of firms on the entity list and other measures to block Chinese access to American technology products and services suggests that the digital divide between the US and China will continue to grow.

For Asia, this is particularly problematic. It may mean that firms in the region have to pick whether to match US tech or Chinese tech standards. Companies in Asia that create new apps, as just one example, are going to be increasingly forced to choose between a US-compatible option or a Chinese one.

Manufacturing firms could face similar obstacles, with increased screening of Chinese involvement and investment, Asian firms could find themselves having to be much more wary about vendors and suppliers.

There are likely to be additional opportunities and challenges coming to Asia in the wake of Phase 1, as firms assess and reassess their options. The agreement, less of a “truce” than a postponement of additional escalation, does not just affect firms in the US and China. Ongoing trade tensions will continue to impact businesses across Asia for 2020 and beyond.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).

Author

Deborah Elms

Dr. Elms is Head of Trade Policy at the Hinrich Foundation in Singapore. Prior to joining the Foundation, she was the Executive Director and Founder of the Asian Trade Centre (ATC). She was also President of the Asia Business Trade Association (ABTA) and the Board Director of the Asian Trade Centre Foundation (ATCF).

Have any feedback on this article?